Rural and Empowered: Countryside Transformation with Rural Bank of Maddela

Rural Bank of Maddela (Quirino) Inc. (RB Maddela), located in the Province of Quirino, has been serving their clients for 44 years. The bank’s long-standing experience did not spare it from the challenges of outdated systems and work processes such as: manual computations, time-consuming report generation, inefficient management and tracking of customer information files with other bank records, slow backup process and no updated customer’s information.

Despite these challenges, rural banks like RB Maddela are resilient even with the ongoing COVID-19 pandemic. Former BSP Governor Benjamin Diokno conveyed that rural banks are sufficiently capitalized to weather the economic crisis caused by the pandemic. The rural banking industry was able to keep up with the increase in credit applications and loan disbursements from the agricultural and healthcare sectors despite strict community quarantine.

For RB Maddela, it was able to productively continue providing loans and other financial services to farmers, jeepney and tricycle drivers, and MSMEs. However, the use of an outdated system limited their capabilities in serving the community better.

The Need for Digitalization

The pandemic has boosted digitalization across all industries, including the banking and finance industry. One example is the Digital Payments Transformation Roadmap 2020-2023 by the Bangko Sentral ng Pilipinas (BSP). The BSP aims to onboard 70% of Filipino adults to the formal financial system through the use of payment or transaction accounts and convert 50% of the total volume of retail payments into digital.

Prior to the pandemic, the rural bank industry had already been preparing for a large-scale digital transformation. In 2018, the Rural Bankers Association of the Philippines (RBAP) and its member banks were working on shifting to digital cloud-based core banking technology, in line with BSP Circular 8080 (Guidelines on Information Technology Risk Management for All Banks and Other BSP Supervised Institutions issued in 2013). The shift in cloud-based core banking systems is seen as a foundational enabler that helps banks like RB Maddela not just to comply with existing and revised regulations but also scale up operations. The cloud-based system further addresses the digitalization challenges banks experience:

Manual computations

The bank performs their computations manually. For example, to generate the Effective Interest Rate (EIR), they input the data into an excel file. Once the EIR is generated, RB Maddela can proceed to compute their monthly amortization in a separate file. Afterwards, the bank will double check their EIR file to ensure that the amortization computation is aligned with it.

Time-consuming report generation

Accounting reports, internal reports, and regulatory reports are all done manually. The bank’s tellers, cashiers, accountants, and compliance personnel have to often work overtime to submit the reports on time.

Inefficient management and tracking of customer information file and other bank records

RB Maddela had a manual file keeping system to track their customers’ and bank records. Due to this, the bank had difficulty locating client records, especially when there is a need to check how often customers pay their loans, if they pay on time or if they have past due payment, and other transactions.

Slow backup process

It usually takes the bank around 30 minutes to an hour to back up its files. If the computer’s storage is full, the bank has to bring their hard drive to the Cauayan office, which is an estimated 2-hour drive. To reduce the size of the files or update the hard drive, they need to go through this tedious procedure.

Unable to edit or update customer’s information

With its current system, RB Maddela would need to update their customers’ information file on certain occasions. For example, if one customer gets married and the person wishes to update his/her file, the bank must create a new account with the updated information. This account will be used to process and log future transactions to replace the previous account.

Through digitalization, the bank can fulfill their mission in helping improve the quality of life in rural areas by delivering quality services in their community.

The Rural Bank of Maddela’s Transformation Journey

RB Maddela started its onboarding to PearlPay’s Core Banking Solution (CBS) on May 13, 2020. Due to social distancing protocols, the bank underwent a virtual onboarding process. All of the training sessions and meetings were done online. Though the shift to digital may be overwhelming, RB Maddela took the change in stride and was able to understand what it takes to fully transform – especially since the bank wasn’t familiar with using digital platforms like Google Meet and Google Drive at the start.

Shifting from traditional banking to a cloud-based banking solution may be a challenging task at first for rural banks. However, digital transformation does not simply mean improving the bank’s infrastructure and system. Digital transformation most significantly means caring for the customers and other stakeholders. For all this development to happen, banks must be open to digitalization and are willing to welcome new ways of doing banking positively.

The onboarding process helped RB Maddela understand and embrace digitalization better. “They provided almost all of everything we needed. We commend their 100% support and guidance to RB Maddela from the start and up to now,” stated Joseph Lejano, President of Rural Bank of Maddela (Quirino), Inc.

First, the bank conducted a gap analysis to identify problems in its current system. The identified gaps were addressed in PearlPay CBS to guarantee that the platform can cater to their needs. This is followed by a series of BSP-mandated compliance checks and data security checks to ensure the system’s compliance.

The next step of the onboarding process was the migration stage where the processes and workflows from the old system were transferred and built into the PearlPay CBS. Afterwards, RB Maddela completed the User Acceptance Testing (UAT) training. It’s an extensive series of learning sessions for core members of the rural banks, typically those involved with IT, compliance, and other managerial positions to familiarize themselves with using the CBS platform. The UAT sessions help transform the bank’s core teams from learners to leaders. Eventually, they can teach their colleagues how to use the CBS.

Once comfortable and assured with the use of CBS, the rest of the employees underwent a series of End-User-Training (EUT) sessions led by RB Maddela’s core team members. This allowed the employees to accept the system as their own and acknowledge the significant milestone in RBM’s digital transformation journey. The EUT sessions and training guaranteed RB Maddela’s efficient transformation despite the lack of IT background among its people and absence of a Tech Team in the bank.

For a certain period, the bank tested its old system and PearlPay’s CBS simultaneously. This allowed a proper and smooth transition from the bank’s old system to the new one.

The Better Way to Transform

RB Maddela officially went live with PearlPay CBS on September 1, 2021. The bank has made remarkable leaps in its employee performance and overall digital transformation journey. With a compliant system that offers streamlined processes, the bank can now do its computations seamlessly and submit reports on time.

“With CBS, we can say that daily bank transactions become easier and faster. Everything in just a click.” -Joseph Lejano, President of Rural Bank of Maddela (Quirino) Inc.

The bank now spends less time processing loans, now able to review loan applications and release loan disbursements more efficiently. Before, RB Maddela had to look for customers’ application forms and manage manually-submitted requirements. Now, everything can easily be searched for in the CBS.

Moreover, RB Maddela is able to train new employees faster. The bank found it easier to learn and adapt using the system than expected. With a more optimized system as well as banking processes, RB Maddela is able to speed up their methods and serve more Filipinos in Quirino and the surrounding locales.

In today’s modern world, it’s easy for traditional financial institutions and businesses to get left behind. Through innovative and affordable digital solutions, the Philippines can rise from underdevelopment. By making financial services universally accessible, more Filipinos can be given the opportunity to succeed and make an impact in their own small or big way.

Digitizing MSMEs: How You Can Grow and Thrive in the Philippine Digital Economy

Photo courtesy of BIMP EAGA Asia Website

Micro, small, and medium enterprises (MSMEs) make up 99.5% of businesses in the Philippines. They play a vital role in the Philippine economy, contributing to 62.66% of employment and 40% of the country’s GDP (as of December 2021). With the rise of COVID-19 in 2020, digitalization in the country improved as several businesses shifted online to reach and serve more people.

MSMEs also have an important role in our country’s economic recovery. They provide more jobs to Filipinos, reach and serve people easily in rural and marginalized communities, and facilitate local economic development throughout the country.

However, 73% of MSMEs experience difficulties on how to go digital due to the challenges that they experience:

Lack of access to credit

Majority of them are unbanked, have no credit history, no assets for collateral, and lack requirements that big financial institutions consider as “high risk” when applying for a loan.

Another challenge is the slow loan approval process. According to Asia Development Bank (ADB), 16% of MSMEs applied for loans in banks during the pandemic but only 4.8% were approved. As one of the heavily impacted sectors by the pandemic, having enough funds is important for small businesses to sustain their livelihood. Without enough funds, they can’t access solutions that can digitize their business.

Slow digital adoption due to slow or unstable internet access

It’s no secret that the Philippines has one of the slowest internet, ranking 68 out of 120 countries in the Inclusive Internet Index 2021. This caused a digital gap in various places in the country – especially between rural and urban communities. With slow and unstable internet, businesses will have a hard time accessing solutions that can help them shift online and participate in the digital economy.

Lack of knowledge and familiarity with using digital solutions

The Philippines is still dependent on manual operations, using paper and pen for inventory and cash transactions for purchases. Plus with slow digital adoption, it’s no wonder that a lot of business owners remain unaware and unfamiliar with the right solutions they can use to digitize their business.

Digitizing MSMEs has the potential to help our country recover from the pandemic and encourage sustainable economic growth but their growth remains limited because of these challenges. What can we do to support the growth of MSMEs in the digital economy?

How MSMEs Can Go Digital and Grow Their Business

First, let’s address how MSMEs can get access to credit for their digitalization. Aside from big banks, small businesses can also apply for loans in rural banks, microfinancing institutions, and cooperatives. These are community-based financial institutions (CBFIs) that provide more affordable loans to MSMEs:

Photo courtesy of Rural Bank of Maddela, Rural Bank of Pagadian, Rural Bank of Cuyo, SIDC, Manila Bulletin, PDIC, and Moneysense

The government also partnered with CBFIs to widen the reach of their MSME financial programs. The Small Business Corporation partnered with the Cooperative Development Authority (CDA) to make Pondo sa Pagbabago at Pag-asenso (P3) more accessible to the sector. They also have MFI and rural bank partners not just for this program but for other financing programs as well. Through these loans, MSMEs can have enough capital to make their business digital.

What about their digitalization challenges?

To address these challenges, the government launched several programs to make digital transformation more accessible to the sector. The Department of Science and Technology launched the Small Enterprise Technology Upgrading Program (SETUP). It’s a nationwide initiative that provides MSMEs access to new technologies and technical, digital, and other critical support. Meanwhile, the Department of Trade and Industry (DTI) created the Ctrl+Biz Reboot Now program that offers businesses a series of free webinars to learn and understand how MSMEs can go digital.

Aside from that government initiatives, there are also accessible and affordable digital solutions that can make them more resilient and competitive in today’s digital economy.

As some businesses went online, they used a digital payment solution to accept e-wallet, mobile banking, QR payments, and other online payments. This allowed their customers to buy and pay online more securely and ensure that their business can continue operating even with social restrictions in place.

There’s also a bills payment platform that can help MSMEs earn more and expand their business. Instead of just accepting payments for their products or services, they can also process bills payment, government contributions, and other transactions in their store. This makes payments easier and more convenient for Filipinos.

By delivering the right solutions, we can unlock the full potential of MSMEs in the Philippines.

How Digital Transformation Benefits MSMEs: Encouraging Sustainable and Long-Term Growth

Photo courtesy of Araneta City and Manila Bulletin

As Enrico Gaveglia, Officer-in-Charge of UNDP Philippines said: MSMEs play a crucial role in the Philippines’ efforts to recover from the crisis brought by the pandemic.

They have provided for the needs of their communities which can be purchased and paid online. By helping them go digital, they can earn more and be more accessible by connecting and serving more Filipinos online. This can encourage more economic activities, especially in rural and marginalized communities, and keep up with big businesses in the long run.

Through digitalization, we can ensure the overall growth of the sector and that no MSME is left behind in the Philippine digital economy.

Manila’s 35 Fastest Growing FinTech Startups

This was originally published on Fintech Energy

At Fintech Energy we track over 200,000 fintech startups and over 1,000,000 people who hold key positions in these companies. We use this directory of startups to highlight top employees, founders and organizations we think deserve more appreciation than they are currently getting.

We’ve ranked the top 35 FinTech companies in Manila. The companies, startups and institutions listed in this article are all exceptional companies, well worth a follow. We have included links to their websites, socials and CrunchBase (if you’re interested in their financials).

We selected the organizations listed in this article based on:

- Track record

- Executive leadership

- Market share

- Innovation

- ESG rating

Our Data – We source our data from OSINT (open source intelligence) and public directories such as Crunchbase, SemRush and many more. The data from these sources should be treated with a degree of caution and verified yourself.

Top FinTech Companies & Startups (Manila)

Acudeen Technologies

Founders: Mario Jordan Fetalino, Mario Salazar

Acudeen is an online technology platform that connects small and medium enterprises to financial institutions through invoice discounting.

PawnHero

Founders: David Margendorff, Manny Ayala, Nix Nolledo

PawnHero – the 1st online pawnshop in the Philippines.

Y Finance Inc.

Founders: Roger Yang

Provides an online lending platform geared towards financial inclusion for all Filipinos.

TendoPay

Founders: Jan Walczak, Kacper Marcinkowski, Kamil Charazka, Timothee Grassin

Tendopay provides Filipinos with alternative payment options for online shopping.

JazzyPay

Founders: Joshua Marindo, Kathleen Acosta

Revolutionizing online payments for businesses of all sizes.

Tagcash

Founders: Mark Vernon

Tagcash is a fintech-enabled app where users can create mini-programs utilizing financial technology and other core features of a wallet.

Saphron

Founders: Francisco Reyes

Making insurance radically accessible to propel financial inclusion.

Satoshi Citadel Industries

Founders: Jardine Gerodias, John Bailon, Miguel Cuneta

Satoshi Citadel Industries is a FinTech startup company that builds Bitcoin solutions to reduce the costs of using and transferring money.

Bloom

Founders: Israel Keys, Justin David, Ramon Tayag

Bloom makes money smarter by combining modern technologies like cryptocurrency with traditional infrastructure.

NextPay

Founders: Aldrich Tan, Don Pansacola

NextPay is a digital banking platform for small businesses and entrepreneurs.

Uploan

Founders: Benoit Portoleau-Balloy, Liam Grealish

Uploan provides an end-to-end salary loan management platform to employers.

Lendeez

Founders: Sagit Attar, Zohar Friling

Mobile financial service for social lending, AI enabling end-to-end management of digital lending between friends and family.

Finscore

Founders: Diana Krumova

Helps first-time borrowers to get access to credit and banks and FIs get more data & insights through smart credit scoring.

Metrobank

Founders: Jobo G. Virtucio III

Metrobank is a financial service company that offers banking services to large local and multinational corporations.

First Digital Finance

Founders: Georg Steiger

A Fintech company in South East Asia, operating the BillEase Buy Now, Pay Later service.

Investagrams

Founders: JC Bisnar, John Michael Mangahas Lapina

Investagrams is an app to invest in the stock market.

Moola Lending

Founders: Unknown

Moola Lending is a financial technology company powered by the Doctor Cash international line of fintech companies.

PearlPay

Founders: Pio Ryan Lumongsod

PearlPay is a Philippine-based Fintech company offering affordable and secured end-to-end banking solutions.

Salarium

Founders: Judah Hirsch

Salarium is a payroll automation platform covering the complete solution from time & attendance, computation, disbursement and compliance.

Coindrop

Founders: Unknown

Coindrop provides access to various financial verticals chosen by enterprise HR to selected employees.

PesoPay

Founders: Joseph Chan

PesoPay is a comprehensive and secure online payment gateway.

Navegar

Founders: Unknown

A Philippines-based private equity fund.

Encash

Founders: Unknown

Encash ATMs in the rural areas makes it possible for the underserved to finally have convenient access to their finances.

Rebit

Founders: Jardine Gerodias, John Bailon, Luis Buenaventura, Miguel Cuneta

Rebit.ph is a service of Satoshi Citadel Industries, a Philippine-based holdings company for Bitcoin-related ventures.

Metrobank Card

Founders: Unknown

Metrobank Card Corporation’s core credit cards provide increased spending power and worldwide purchasing convenience.

VMoney Inc.

Founders: Unknown

VMoney Inc. is a financial technology company that develops, operates, and markets payment processing solutions.

Banana Pay

Founders: Unknown

Banana Pay is a mobile application that specializes in financial services.

Vesl Trade Finance

Founders: Maureen Nova Ledesma

Vesl is an information technology company that provides a software platform that connects lenders and businesses online.

Paywise

Founders: Sazzad Khan

Paywise in Fintech newest innovation.

Moneygment

Founders: Unknown

Moneygment is an app for financial transactions, social literacy, and digitalization.

Packworks

Founders: Bing Tan, Hubert Yap, Ibba Bernardo, Julian Legazpi

Our mission is to help millions of micro-entreps in the ASEAN grow their business by providing them with tools, insights, and access.

CreditPros

Founders: Unknown

CreditPros is a financial company that provides personal loan, loan for autonomous and employees.

Mount Fuji Lending, Inc.

Founders: Aoi Ikeda, Gene Frizzell

We’re transforming the Philippine’s B2B lending industry through tailoring, relationships, and fintech.

Orcestra

Founders: Unknown

Orcestra provides revenue, cost control, cloud and security solutions for banks and financial institutions to boost operation and profits.

MSME Financial Support Programs

{kind=link}

{kind=link}

{kind=link}

Programa ng SBCorp na naglalayon na suportahan ang mga maliliit na negosyo sa pamamagitan ng pagbigay ng loan na may interes na hindi hihigit sa 2.5% kada buwan.

- Makakakuha ng loan mula P5,000 hanggang P200,000

- Maliliit na negosyong tumatakbo na hindi bababa sa 1 taon

- Rehistrado sa DTI, munisipyo, o barangay

- Hindi hihigit sa P3 milyon ang asset

a. Online Application Form

b. Rehistro ng Negosyo/DTI Business Name Registration

c. Kopya ng Valid ID

d. Barangay Clearance

e. Katibayan na tumatakbo ang negosyo na hindi bababa sa 1 taon

f. Permit mula sa barangay o munisipyo

g. ID picture

1. Ihanda at i-scan ang mga dokumento (.jpeg format).

2. Pumunta sa link na ito: brs.sbcorp.ph.

3. Gumawa ng account at piliin ang angkop na loan program.

4. Sagutan ang online application form.

5. Antayin ang kumpirmasyon na natanggap ang iyong application at ang resulta nito na ipapadala sa e-mail.

Rise Up Multipurpose Loan

Programa ng SBcorp na naglalayon na magpautang ng may maluwag na loan terms para mas mapadali ang access ng mga maliliit na negosyo sa credit at tulungan silang maka-recover mula sa pandemya. Ang programang ito ay mayroong tatlong uri ng loan:

- Micro Multi-Purpose Loan - maaaring humiram ng hanggang Php300,000. Mababayaran ito kada buwan sa loob ng 3 taon at mayroong grace period na hanggang 12 buwan.

- SME Multi-Purpose Loan Suki - maaaring humiram ng hanggang P5.0 million for *clean loan. Mababayaran ito kada buwan sa loob ng 5 taon at mayroong grace period na hanggang 12 buwan.

- SME Multi-Purpose Loan First Timers - maaaring humiram ng hanggang P3.0 million. Mababayaran ito kada buwan sa loob ng 3 taon at mayroong grace period na hanggang 12 buwan.

*Ang clean loan ay loans na hindi kailanman nag-default, nag-prepaid o na-claim sa buong loan payment term.

Maaari mag-apply ang sumusunod na negosyo sa iba’t ibang uri ng loans sa ilalim ng Rise Up Multipurpose loan:

- Micro Multi-Purpose Loan - Para sa mga maliliit na negosyo

- SME Multi-Purpose Loan Suki - Para sa kasalukuyang borrowers ng SBCorp na may hindi bababa sa 6 na buwan na may magandang track record ng pagbabayad.

- SME Multi-Purpose Loan First Timers - Para sa maliliit at medium-sized na negosyo.

- Government-issued ID

- Barangay Micro Business Enterprise (BMBE) Certificate o Mayor’s Permit

- Mga larawan at video ng business operations at assets

- Corporate documents kung applicable (ex. Secretary’s Certificate, Partnership Agreements, Business License and Registration atbp.)

- Business Track Record na hindi bababa sa isa o tatlong taon (depende sa uri ng loan) bilang ebidensya ng mga business permit.

Paalala: May mga karagdagang requirements na dapat isumite depende sa uri ng loan na iyong a-applyan. Bisitahin ang https://sbcorp.gov.ph/riseupmultipurpose/ para sa karagdagang detalye.

1. Pumunta sa https://brs.sbcorp.ph at mag log-in o gumawa ng account.

2. Pagkatapos mag login, pindutin ang Apply for a loan.

3. Piliin ang RISE UP Multi-Purpose Loan sa mga available na loan program.

4. Pindutin ang First-Time Borrower sa lumabas na mensahe kung ikaw ay first time borrower, kung hindi mag patuloy lang sa application process.

5. Sagutan ang registration form at i-upload ang mga kinakailangan na documents.

6. Pindutin ang Submit upang matapos ang application process.

Rise Up Tindahan Loan

Programa ng SBcorp na nagbibigay access sa credit sa mga sari-sari store, retail store, dealer, at distributor na bahagi ng network partner ng Fast Moving Consumer Goods (FMGCs). May dalawang uri ng loan sa programang ito:

- Micro Tindanan Loan - maaaring humiram ng hanggang P300,000. Mababayaran ito kada buwan sa loob ng 3 taon at mayroong grace period na hanggang 12 buwan.

- SME Tindahan Loan - maaaring humiram ng hanggang P5 million. Mababayaran ito kada buwan sa loob ng 3 taon at mayroong grace period na hanggang 12 buwan.

- Dapat ay 100% Filipino-owned para sa sole proprietorship (negosyo na 1 tao ang may-ari) o partnership (negosyo na may 2 o mas higit pa na may-ari). Hindi bababa sa 60% Filipino-owned MSME para sa korporasyon.

- Kailangang may asset size na hindi hihigit sa P100 milyon (hindi kasama ang halaga ng lupa)

- Dapat ay kasali sa supply chain kasama ang isang SBCorp- accredited FMCG na kompanya ng hindi bababa sa 1 taon

- Dapat ay walang past due account/s sa alinmang SBCorp lending program

Maaaring mag-apply ang mga negosyo sa sumusunod na loans:

- Micro Tindanan Loan - para sa mga sari-sari store na may FMCG accreditation

- SME Tindahan Loan - para sa mga retail stores, dealers at distributors na may FMCG accreditation

- Government-issued ID

- Barangay Micro Business Enterprise (BMBE) Certificate o Mayor’s Permit

- Mga larawan at video ng business operations at assets

- Corporate documents kung applicable (ex. Secretary’s Certificate, Partnership Agreements, Business License and Registration atbp.)

- Proof of Asset o katibayan ng asset na hindi hihigit sa Php 100 na milyon

Paalala: May mga karagdagang requirements na dapat isumite depende sa uri ng loan na inyong a-applyan.

1. Pumunta sa https://brs.sbcorp.ph at mag log-in o gumawa ng account.

2. Pagkatapos mag-login, pindutin ang Apply for a loan.

3. Piliin ang angkop na loan sa mga available na loan program.

4. Sagutan ang registration form at i-upload ang mga kinakailangan na documents.

5. Pindutin ang Submit upang matapos ang application process.

Programa ng SBCorp na naglalayong makatulong sa puhunan at pagpapalago ng mga maliliit na negosyo at mapaigting ang supply chain ng pagkain at magbigay ng loan na walang interes at kolateral.

- Makakakuha ng 2% ng isang taong benta

- 3 buwang repayment term

- 3% service fee

- Makakakuha ng 2.25% ng isang taong benta

- 4 na buwang repayment term

- 3% service fee

- Makakakuha ng 2.25% ng isang taong benta

- 4 na buwang repayment term

- 3% service fee

- Mga negosyo na nasa sektor ng pagkain o bahagi ng supply chain ng SBCorp-accredited fast-moving consumer goods (FMCG) food manufacturer

- Kung hihiram nang mas mababa sa P1 milyon: may magandang pampinansyal na katayuan ang negosyo sa nakaraang taon

- Kung hihiram nang higit sa P1 milyon: may magandang pampinansyal na katayuan sa nakaraang 3 taon

- Walang natitirang negatibong utang ang aplikante at ang negosyo sa ibang loan program o pampinansyal na institusyon

Para sa maliliit na sari-sari stores:

a. Government-issued ID

b. Bank account o electronic money account

c. 2019 at 2020 Barangay Business permit

d. 2 larawan ng karatula ng negosyo at mga inventories, o fixed assets (.jpeg format)

Para sa mga malalaking sari-sari stores/ mini groceries/ convenience stores:

a. Government-issued ID

b. Bank account o electronic money account

c. 2019 at 2020 Mayor’s Permit

d. 2 larawan ng karatula ng negosyo at mga inventories, o fixed assets (.jpeg format)

Para sa mga medium-sized grocery/convenience stores; dealers at maliliit na distributors:

a. Government-issued ID

b. Bank account o electronic money account

c. 2018, 2019, at 2020 Mayor’s Permit

d. Para sa mga uutang ng P10 milyon pataas – pinakabagong BIR-filed Balance Sheet ng negosyo upang masigurado na ang negosyo ay medium-sized

e. Para sa mga korporasyon at mga partnerships/may kasosyo lamang – Secretary’s Certificate (awtorisasyon na ang Presidente/CEO ng negosyo o ang katumbas nitong posisyon ay ang prinsipal na hihiram)

1. Ihanda at i-scan ang mga dokumento (.jpeg format)

2. Pumunta sa link na ito: brs.sbcorp.ph .

3. Gumawa ng account at piliin ang angkop na programa.

4. Sagutan ang online application form.

5. Antayin ang ipinadalang kumpirmasyon na natanggap ang iyong application at ang resulta nito sa e-mail.

Programa ng PhilGuarantee na naglalayong makapagbigay ng risk guarantee sa mga maliliit na negosyo upang matulungan silang magkaroon ng puhunan.

- Guarantee limit na 50% ng prinsipal na utang

- 1 taong guarantee term o panahon na kailangan mabayaran nang buo ang nakuhang guarantee

- 1-5 taon na loan term

- Guarantee fee: 1% kada taon + gross receipt taxes (GRT)

- Amendment fee: P5,000 kada pagbabago sa napagkasunduan

- Walang origination fee

Maaaring humiram ang mga maliliit na negosyo na may hindi hihigit sa P100 milyon ang asset at naapektuhan ng pandemya.

1. Alamin ang requirements na kailangan ng iyong paga-applyang PhilGuarantee-accredited lending na bangko o pampinansyal na institusyon.

2. Magpasa ng aplikasyon at mga requirements sa mga PhilGuarantee-accredited lending na bangko o pampinansyal na institusyon.

3. Kukunsultahin ng PhilGuarantee ang bangko o institusyon ang pag-apruba ng guarantee coverage. Antayin ang resulta mula sa PhilGuarantee.

Programa ng SBCorp na naglalayong suportahan ang mga maliliit na negosyong panturismo, DOT-accredited man o hindi.

- Makakakuha ng hanggang P5 milyon

- Loan term: kada buwan hanggang 4 na taon

- Grace period*: hanggang kalahati ng loan term (multiples ng 3 months option) sa prinsipal na utang

- Interes: one-time service fee na 4% - 8%, depende sa repayment term

Note: Grace period: panahon kung saan walang multa na kailangang bayaran kung sakaling hindi makapagbayad sa tamang oras.

- Makakakuha ng hanggang P300,000

- Loan term: kada buwan hanggang 4 na taon

- Interes: one-time service fee na 4% - 8% depende sa repayment term

Maaaring humiram ang mga maliliit na negosyo (MSMEs) na kabilang sa mga tourism enterprises o tourism support services na tumatakbo ng isang taon.

a. Government-issued ID

b. Barangay Permit

c. Barangay Micro Business Enterprises (BMBEs) permit o Mayor’s Permit

d. Isang (1) minutong bidyo ng operasyon ng negosyo at mga dokumento ng asset, kung mayroon

1. Ihanda at i-scan ang mga dokumento (.jpeg format).

2. Magtungo sa link na ito: brs.sbcorp.ph/

3. Gumawa ng account at piliin ang angkop na programa.

4. Sagutan ang online application form.

5. Antayin ang kumpirmasyon na natanggap ang iyong application at ang resulta nito na ipapadala sa e-mail.

Programa ng SBCorp na naglalayong makapagbigay ng kapital na pangnegosyo sa mga pinabalik o napabalik na mga OFWs dahil sa pandemya.

- Loan amount mula P30,000 - P100,000

- 12 months grace period*

- Walang interes

- Walang kolateral

Note: Grace period: panahon kung saan walang multa na kailangang bayaran kung sakaling hindi makapagbayad sa tamang oras.

a. Sertipiko ng pagkumpleto ng Philippine Trade Training Center (PTTC) online training session

b. Video presentation (ipapaliwanag sa PTTC)

c. Scanned copy ng passport

d. Para sa hihiram ng higit sa PhP50 libo – Business Model Canvas

1. Tapusin ang online training na pamamalakad ng Philippine Trade Training Center (PTTC). Pwedeng mag-register sa link na ito: HEROES Pre-Registration Form.

2. Pagkatapos mag-training, ihanda ang mga dokumentong hinihingi.

3. Pumunta sa brs.sbgfc.org.ph heroes upang magpatuloy sa application.

Programa ng LANDBANK at OWWA na naglalayong makapagbigay ng loan na pangnegosyo sa mga OFWs.

- Para sa mga sole proprietorship/nag-iisang may-ari: makakakuha ng P100,000 hanggang P2 milyon

- Para sa mga partnerships/may kasosyo, korporasyon, at kooperatiba: makakakuha ng P100,000 hanggang P5 milyon

- 7.5% interes kada taon

- Loan term

- - Short term: hanggang 1 taon

- - Long Term: hanggang 7 taon kasama na ang 2 taon na grace period*

- Kolateral: asset ng negosyo katulad ng makina at mga equipment

Note: Grace period: panahon kung saan walang multa na kailangang bayaran kung sakaling hindi makapagbayad sa tamang oras.

- OFW na miyembro ng OWWA

- Nakatapos ng Enhanced Entrepreneurial Development Training

- Kung may asawa: kanyang legal na asawa

- Kung byudo/byuda, walang asawa, o hiwalay sa asawa: kanyang magulang (kung hindi pa 66 taong gulang o mas matanda pa) o ng kanyang anak (hindi bababa sa 18 taong gulang)

a. Sertipiko mula sa OWWA na ikaw ay isang OFW

b. Sertipiko ng pagkumpleto ng Enhance Entrepreneurial Development Training (EEDT)

c. Business Plan/Proposal

d. 2 valid ID na may pirma

e. Statement of Asset and Liabilities

f. Proof of Billing Address

g. Certificate of Residency galing sa Barangay

h. Drawing o sketch ng lugar kung saan nakatira

Para sa mga OFWs na mayroon nang negosyo bago pa mag-apply:

a. Rehistro ng DTI

b. Bio-data ng aplikante

c. Mayor’s permit

d. Kung may contract growing agreement: Income Tax Return ng nakaraang 3 taon, BIR-filed Financial Statements ng nakaraang 3 taon, at ang pinakabagong Interim Financial Statement

Programa ng LANDBANK at OWWA na naglalayon makapagbigay ng oportunidad sa pagnenegosyo at tulong-pinansyal sa mga OFWs.

- Para sa mga sole proprietorship/nag-iisang may-ari: makakakuha ng P100,000 hanggang P2 milyon

- Para sa mga partnerships/may kasosyo, korporasyon, at kooperatiba: makakakuha ng P100,000 hanggang P5 milyon

- 7.5% interes kada taon

- Loan term

- - Short term: hanggang 1 taon

- - Long term: hanggang 7 taon kasama na ang 2 taon na grace period*

- Kolateral: asset ng negosyo katulad ng makina at mga equipment

Note: Grace period: panahon kung saan walang multa na kailangang bayaran kung sakaling hindi makapagbayad sa tamang oras.

a. Application Form

b. Sertipiko ng pagkumpleto ng Entrepreneurial Development Training

c. Kopya ng rehistro sa DOLE, SEC o CDA

d. Sertipiko mula sa Regional Welfare Office (RWO) Director na ang aplikante ay isang tunay na OFW at kinikilala ng OWWA

e. Beneficiary Profile

f. Business Permit

g. Business Plan o proposal na nagpapakita na ang equity ay kasing halaga ng 20% ng kabuuang project cost

h. Board resolution na nagtatalaga ng business manager na awtorisadong mag-apply sa ngalan ng organisasyon

Programa ng ACPC na naglalayong magbigay ng loan na walang interes sa mga OFWs na nawalan ng trabaho dahil sa epekto ng COVID-19 pandemic.

- Micro Agri-Negosyo Loan: makakakuha ng hanggang P300,000

- Small Agri-Negosyo Loan: makakakuha ng P300,000 hanggang P15 milyon

- Lending partners: Government Financial Institutions (GFIs) at Non-Government Financial Institutions (NGFIs)

- Hanggang 5 taon na loan term

- Mga may-ari o miyembro ng mga maliliit na negosyo mula sa mahihirap na sektor at maliliit na magsasaka at mangingisda

- Rehistrado o enrolled sa Registry System for Basic Sectors in Agriculture (RSBSA). Maaaring magparehistro sa RSBSA sa Municipal Agriculture Office (MAO).

1. Alamin ang requirements na kailangan ng iyong paga-applyang bangko o partner lending conduit (PLC)

2. Mag-sign up at magbukas ng account sa https://acpcaccess.ph/.

3. Mag-schedule at dumalo sa online program briefing.

4. Piliin ang loan facility (ANYO) at kumpletuhin ang requirements.

5. Mag-schedule at dumalo sa Business Planning Workshop.

6. Ipo-proseso at susuriin ng PLC ang iyong loan application.

Programa ng ACPC naglalayong makapagkaloob ng puhunan pangnegosyo sa mga kabataang entrepreneurs at nakapagtapos ng kursong agri-fishery sa pamamagitan ng pagbibigay ng walang interes na pautang.

- Makakakuha ng hanggang P500,000

- Hanggang 5 taon na loan term

- Agripreneur na may edad na 18 - 30 taong gulang

- Nakapagtapos ng kursong kaugnay sa agri-fishery (diploma) o nakakumpleto ng training course (certificate of completion)

- Rehistrado sa Registry for Basic Sectors in Agriculture (RSBSA) o sa Farmers and Fisherfolk Enterprise Development Information System (FFEDIS).

a. 1 valid government-issued ID na may larawan ng aplikante

b. Application form

c. Simpleng business plan

d. Sertipiko ng pagtatapos ng kursong kaugnay sa agri-fishery o pagkakakumpleto ng training

1. Mag-sign up at magbukas ng account sa acpcaccess.ph.

2. Mag-schedule at dumalo sa online program briefing.

3. Piliin ang loan facility (KAYA) at kumpletuhin ang mga requirements.

4. Mag-schedule at dumalo sa Business Planning Workshop.

5. Iprepresenta ang business proposal mo at ilalapit ka sa kanilang partner lending institution.

6. Ipoproseso at susuriin ang iyong loan application.

Programa ng ACPC na naglalayong makapagbigay ng walang kolateral at interes na pautang sa mga maliliit (micro at small) na agripreneurs na naapektuhan ng enhanced community quarantine (ECQ).

- Makakakuha ng hanggang P10 milyon

- Hanggang 10 taong loan term

Notes: Maaaring humingi ng maliit na fee ang ibang partner lending institutions.

- Handang mag-deliver o mag-supply sa DA-KADIWA Ni Ani at Kita centers at mga lugar na may malakas na pagkonsumo katulad ng Metro Manila at iba pang demand centers

- Rehistrado sa CDA, SEC o DOLE

- Hindi bababa sa isang 1 taon na tumatakbo ang negosyo

a. Letter of Intent na may paglalarawan ng proyekto

b. Registration documents

c. Financial statement

d. Endorso mula sa Department of Agriculture

1. Mag-sign up at magbukas ng account sa acpcaccess.ph/.

2. Mag-schedule at dumalo sa online program briefing.

3. Piliin ang loan facility (SURE COVID-19) at kumpletuhin ang mga kinakailangan na dokumento.

4. Mag-schedule at dumalo sa Business Planning Workshop.

5. Iprepresenta ang business proposal mo at ilalapit ka sa kanilang partner lending institution.

6. Ipoproseso at susuriin ang iyong loan application.

Programa ng SBCorp na naglalayong matulungan ang mga maliliit na negosyo sa kanilang mga pangangailangan sa negosyo sa pamamagitan ng direct lending facilities.

- Pantustos sa pambili ng service o delivery vehicle at pagpapaayos o pagpapagawa ng bodega, tindahan, o pagawaan.

- Loan term: 3 - 5 taon

- Kolateral: real estate o chattel mortgage (mga pag-aari na madaling mailipat o maigalaw)

- Pampuhunan o pantustos sa pagbili ng inventory

- 1 taong credit line

- Makakakuha ng hanggang 80% ng receivables o 60% ng inventories

- Karamihan ng asset at equity ay pagmamay-ari ng Pilipino

- May asset na hindi hihigit sa P100 milyon (hindi pa kasama ang halaga ng lupa)

- May magandang pampinansyal na katayuan sa nakaraang 2 taon

- Rehistrado sa DTI o SEC

- Hindi kabilang ang negosyo sa mga sumusunod:

- - Farm level production na may kaugnayan sa agriculture, aquaculture at/o livestock (maliban ang post-production);

- - Real estate development (maliban ang MSME contractors);

- - Pure trading of imported commodities (maliban na lang kung mayroong dagdag na serbisyo na nakakatulong sa lokal na komunidad);

- - May kaugnayan sa bisyo

Kung nais mag-apply at malaman ang mga requirements, tawagan ang retail lending team ng SBCorp:

+63 2 7751 1888 local 1635 (South Luzon at NCR)

(082) 221-1488 (Mindanao)

Programa ng DBP na naglalayong makapaghatid ng tulong-pampinansyal sa mga publiko at pribadong institusyon na naapektuhan ng mga kalamidad (hal. pandemya, bagyo, baha, lindol, tagtuyot, paglaganap ng peste o sakit, kaguluhan, atbp.)

- Makakakuha ng hanggang 95% ng halaga ng nasalantang ari-arian o asset

- Interes: Depende sa pagkukuhaan ng utang

- Loan Term

- - Para sa mga pribadong institusyon: hanggang 10 taon kasama na ang tatlong 3 na grace period*

- - Para sa permanenteng working capital – hanggang 5 taon kasama na ang 1 taon na grace period*

- Kolateral: Real Estate Mortgage (REM), Chattel Mortgage** (CHM), Hold-out on Deposits, atbp.

*Ang grace period ay tumutukoy sa ibinigay na panahon kung saan walang multa na kailangang bayaran kung sakaling hindi makapagbayad sa tamang oras.

**Ang chattel mortgage ay ang pagsasanla o paggamit sa mga pag-aari na madaling mailipat o maigalaw bilang kolateral o loan security.

- Negosyo na tumatakbo ng 1 taon o higit pa bago ito naapektuhan ng kalamidad

- Walang nasuri ang mga bangko at mga major suppliers na ikakasama sa iyong negosyo

a. DBP Application Form

b. Customer Information File Form kasama ang Loan Record Form

c. Financial Statements sa nakaraang 3 taon o iba pang kaugnay na pampinansyal na dokumento

d. Awtoridad para sa bangko na magsagawa ng pagsusuri o pagtatanong at magbigay ng mga impormasyon tungkol sa mga credit sa mga credit bureaus at iba pang bangko at creditors (DBP form)

e. Board resolution na nagtatalaga kung sino ang hihiram at sino ang karapat-dapat pumirma (kung naaangkop)

f. Detalye ng proyekto (kasama ang cost estimate)

g. Business Registration mula sa DTI/SEC/CDA

h. Business Permit mula sa LGU

i. Business/Company profile (kasama ang mga detalye ng subsidiaries at/o affiliates, Board of Directors at management, at Stockholders)

j. Latest General Information Sheet

k. By-Laws at Articles of Incorporation/Cooperation

l. Karagdagang Requirements (kung naaangkop):

- Real Estate Collateral/Security

- 1. 2 kopya ng Location Plan at Vicinity Map

- 2. 2 kopya ng TCT/OCT

- 3. Pinakabagong Real Estate Tax Declaration at Tax Receipt

- Chattel Collateral**

- 1. Affidavit of Ownership at Certification of Non-Encumbrance with specifications

- 2. Suppliers Quotation complete with technical specifications, para sa makina at/o equipment

- 3. Contract to Sell, para sa makina at/o equipment na matatanggap

- 4. Kopya ng OR/CR para sa transportation equipment

- Building rehabilitation

- 1. Bills of Materials at Cost Estimates

- 2. Building Plan at Specification

- 3. Building Permit

1. Pumunta sa pinakamalapit na DBP Lending Center at magbukas ng bank account.

2. Pumunta sa website na https://www.dbp.ph/lending-groups/ upang makita ang mga provincial lending groups.

3. Kailangan i-file ang inyong application sa loob ng 60 na araw simula sa araw na nagdeklara ng kalamidad.

4. Kung sakali man sumasailalim pa rin sa quarantine ang inyong lugar, ang deadline ng application ay dapat 60 araw pagkatapos iangat ang quarantine o mandatory grace period*.

Factors to Consider for Digital Transformation and Growth

The ongoing pandemic showed the importance of digitalization in the Philippines, especially for financial institutions. Both e-wallet accounts and digital payments have skyrocketed in recent months. To address the financial needs of the public, the Bangko Sentral ng Pilipinas (BSP) is working to develop a digital payments ecosystem and prepare Filipinos for the “new economy.”

While more people are now open to using digital solutions, there are still various obstacles that hinder digital transformation. For example, fragmented and outdated infrastructure in the Philippines, makes it harder for rural banks, microfinancing institutions (MFIs), and cooperatives to digitalize.

The Talent Gap and Legacy System as Common Roadblocks

One of the primary challenges in transformation for Fis in the Philippines is lack of technical know-how including the right personnel. To start digital transformation, organizations must have the right talent or resources equipped with IT skills to address key issues in digital transformation successfully.

Likewise, the use of outdated technology makes transformation more challenging. Most financial institutions still operate with legacy systems. These systems are highly complex, outdated, and require high operating and maintenance costs which make it extremely difficult for institutions to transform digitally. With all these challenges, how can financial institutions transform in the philippines?

Factors to Consider for a Successful Digital Transformation of Financial Institutions in the Philippines

Understanding what constitutes successful digitalization is the next crucial step after identifying its roadblocks. Here are the 4 main digital transformation factors that financial institutions need to consider when they start their digitalization journey.

Openness to Change

Before financial institutions can digitalize, an organization-wide mindset shift is needed. Everyone, including managers and personnel, must be open to change. Research suggests that an organization’s openness to change tends to promote higher levels of cooperation and improved employee performance.

Financial institutions must create a culture where employees are ready to be led by specialists and welcome new methods and technologies. This type of culture can speed up their transformation.

Continuous Learning Culture

Employees are given a fundamental role in digitalization. They carry out new technology and introduce it to customers. But in a fast-evolving industry, keeping up with every new digital solution is just impossible. For this reason, employees need to have the right mindset—to be consistently willing to learn new concepts.

Industry leaders believe that constant upskilling is beneficial to employees’ careers and help them adapt to changes in the workplace. When employees have the willingness to learn, institutions must then proactively give them engaging learning opportunities. This will help these institutions reach their goals and improve their business outcomes.

Finding the Right Service Provider

Institutions have the full discretion in choosing the right service provider for their transformation needs. However, they must choose a partner that can equip them with the right solutions to address the digitalization pain points they experience.

With most rural banks, MFIs, and cooperatives not having an IT department, collaborating with the right provider that can guide and support them every step of the way can ensure smooth digital transformation.

Effective Client-Provider Communication

An effective client-provider communication is key for achieving business growth. As financial institutions decide to undergo digital transformation, their providers must be well informed of what they want to achieve. This makes sure that both parties are on the same page and can do what is required toward achieving the goal.

Being upfront and open also encourages feedback from the client. From here, providers can improve the quality of their service further. Effective communication builds trust and maintains a strong client-provider relationship. It also saves time, money, and energy for both parties, ensuring that the time is well spent since it prevents potential confusion between business partners.

As more businesses, organizations, and even individuals are going digital, financial institutions must adapt quickly to the changing financial landscape. For rural banks, MFIs, and cooperatives, digitalization would help them make data-driven decisions that can open up new business opportunities, eventually leading to their growth. By considering these digital transformation factors, we can encourage and help more institutions to transform, serve their communities better, and improve financial access to underserved and unbanked Filipinos.

Contributed by: Glen Cuya

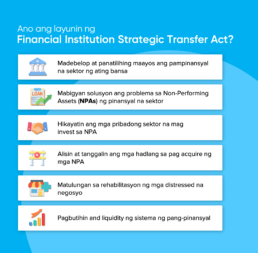

PH COVID-19 Recovery Plan: Financial Institution Strategic Transfer (FIST) Act

The ongoing pandemic affected thousands of businesses and millions of people in the country, prompting the government to develop a recovery plan that can help cushion the impact of COVID-19. One of the programs was the Financial Institution Strategic Transfer Act to help financial institutions recover.

Financial Institution Strategic Transfer (FIST) Act

Republic Act (RA) 11523, also known as the Financial Institution Strategic Transfer (FIST) Act, was signed by President Rodrigo Duterte last February 16, 2021. It aims to ensure financial resiliency during the pandemic by:

- Addressing the non-performing asset problems of the financial sector

- Encouraging the public and private sector to invest in non-performing assets

- Eliminating existing barriers in acquiring non-performing assets

- Helping in the rehabilitation of distressed businesses

- Improving the liquidity of the financial system which can be used to grow the economy and maintain financial stability.

What’s the goal of the Financial Institution Strategic Transfer Act?

The COVID-19 program will facilitate the disposal and transfer of Non-Performing Assets (NPAs) and Non-Performing Loans (NPLs) of the public and private financial institutions by creating a corporation called Financial Institutions Strategic Corporations (FISTC).

Through FISTC, institutions such as commercial banks, rural banks, accredited microfinance nongovernment organizations (NGOs), government financial institutions (GFIs), and other institutions licensed by the BSP can offload their NPAs and NPLs.

This allows financial institutions to provide businesses access to capital and other financial resources. It will help them support their livelihood and stimulate the economy during the pandemic.

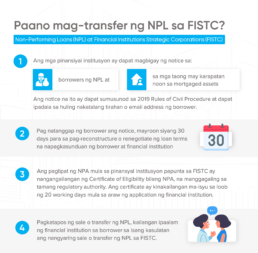

How to Transfer NPL to FISTC

Currently, the country’s non-performing loan ratio is at 4.21% in March 2021 but according to BSP Governor Benjamin Diokno, the banks’ NPLs ratio is expected to be above 6% by the end of December 2021. BSP predicts that within the two-year of implementation of the FIST Act, about 30% of total NPAs will be freed by financial institutions.

Through this program, the financial industry will become protected amid the COVID-19 crisis they are currently facing. The recovery plan will not only help improve the Philippine economy but also provide Filipinos good financial health which is essential to any country.

To read more on different support and assistance provided by the government financial industry to the Filipinos, click here.

Contributed by: Luisa Mae Gonzales

Serbisyo sa Barangay: Livelihood Program for MSMEs

Photo courtesy of Global Giving Website

MSMEs are still recovering from the impact of the pandemic, especially those located in barangays. To support barangay enterprises, the government launched the Livelihood Seed Program – Negosyo Serbisyo sa Barangay (LSP-NSB) to help more than 40,000 MSMEs for this year.

Livelihood Seeding Program – Serbisyo sa Barangay (LSP-NSB)

Photo courtesy from ABS-CBN News, Post Guam Website, and PNA Website

LSP-NSB is a livelihood program by the Department of Trade and Industry (DTI) that provides business development assistance to MSMEs in barangays. It will provide business support to barangays within the 4th, 5th, and 6th classification, encouraging the growth of MSMEs in barangays:

- 4th Class - Municipalities that have an average annual income of more than three million pesos but less than five million pesos.

- 5th Class - Municipalities that have an average annual income of more than one million pesos but less than three million pesos.

- 6th Class - Municipalities that have an average annual income of less than one million pesos.

MSMEs can check with their local Barangay SME Counselor or visit the nearest Negosyo Centers or local DTI Offices if the program is available in their barangay.

Who are qualified to avail the program?

Sole proprietors, cooperatives, and sectoral associations located in barangays may apply for the program. The program is also available for MSMEs in Local Communist Armed Conflict (LCAC) areas and vulnerable communities like Indigenous Peoples (IPs) and refugees or stateless persons.

MSMEs that have been impacted by natural and human-caused disasters, such as diseases and pandemics, will receive priority assistance.

What are the services offered in the program?

Photo courtesy from Daily Tribune, Manila Bulletin, and Punto Website

LSP-NSB aims to increase the awareness of barangay officials about the services that DTI offers and help identify MSMEs operating in barangays. This will allow local government units to provide the needed support to businesses in their communities, such as:

1. Facilitating Business Registration covers business name, Barangay Micro Business Enterprise (BMBE) registration, barangay clearances, and registration with the local government unit, Security Exchange Commission (SEC), Cooperative Development Authority, etc.

2. Business Advisory: includes SME counseling, product development, financing facilitation, market/business matching, trade promotion, and investment promotion.

3. Business Information and Advocacy: provides MSMEs the necessary information, training, seminars, and workshops.

4. Provision of livelihood kits: businesses will receive individual kits worth P5,000-P8,000 to help them restore and improve their livelihood. The type of kit to be provided will depend on the needs of affected MSMEs.

How MSMEs Can Avail the Livelihood Kit

MSMEs have to submit a business name certificate or barangay permit, simplified action plan, pledge of commitment, and attended business development sessions held by the DTI Provincial Offices and Negosyo Centers in their areas to get the livelihood kit.

Photo courtesy from Philippines News, DTI Website and Salay Misor Website

As one of the sectors heavily affected by the pandemic, the livelihood program for barangay MSMEs can help them recover and sustain their business. It will also provide them more opportunities to grow and contribute to the economic development of their barangays in the long run.

If you want to know more about the different government programs for MSMEs, click here!

Contributed by: Mark Goli

Boosting Countryside Development in the Philippines: Livelihood Opportunities for Filipinos

Metro Manila is the most densely populated city in the world with a population of around 14,158,573. Prevalence of rural poverty and the lack of opportunities in provinces continue to force many Filipinos to choose to move to Metro Manila in hopes of a better future. This resulted in overpopulation and a multitude of drawbacks like strained housing, infrastructure, and basic services being offered in the metro.

Other problems include the increase of informal settlements, houses made out of unsafe materials in run-down areas, and increased risk of natural disasters due to their location and limited coping strategies. These conditions only worsened poverty and increased vulnerability of those in the marginalized sector.

To tackle the problem, the Philippine government launched a community development program last year. Known as the Balik Probinsya, Bagong Pag-Asa (BP2) program, it aims to address the congestion issues in urban areas by developing countryside systems and providing better opportunities in provinces. Through the countryside development program, Filipinos no longer have to move to highly urbanized cities in hopes of finding a better job and future.

Balik Probinsya, Bagong Pag-Asa (BP2) Program

The BP2 program seeks to improve the countryside and provide rural communities the same opportunities in urban communities by addressing 4 key areas:

1. The empowerment of local industries in the Philippines

The government will establish various loan facilities and credit funds, livelihood seeding programs, and support services to MSMEs. This will promote regional development and encourage the transfer of medium and large businesses from cities to provinces.

2. Productivity in the food security and agricultural sectors

The rural development program also encourages and facilitates innovations and technologies geared towards modernizing agricultural and agrifishery sectors in provinces. This includes the promotion of new and updated techniques, provision of necessary facilities and equipment to those in need, equipment of necessary skills and support, and enhancement of financial services through digitalization and expansion of existing credit programs.

3. The development of the nation’s infrastructure

The program will identify key production and settlement areas in the country. It aims to link food production areas to residential areas for increased efficiency and accessibility to Filipinos.

4. Improvement of overall social welfare, health, and employment

An additional initiative of the program is to improve local health facilities and services, invest in various learning systems, and provide training to program beneficiaries and equip them with the necessary skills for available jobs in their provinces.

The countryside development program will also empower local government units (LGUs) to manage crises and build resilient communities effectively. Various government agencies will be coordinating with one another to ensure the continuous improvement of rural economies and quality of life in the countryside.

Who are the main beneficiaries of the BP2 program?

Low-income families who decided to go back to their province, lost their jobs or other source of income, live in unsafe dwelling places, and are exposed to health and safety risks and other environmental hazards can apply for the program.

Requirements

Prepare the following documents if you want to apply for the BP2 program:

How to apply for the BP2 Program

There are two ways on how you can register for this program:

Online Application

With the COVID-19 pandemic, the safest and most convenient way to apply for the BP2 program is through their official website. Just fill out the form and submit it online.

LGU Application

You can also go to the nearest barangay office to apply for the government rural development initiative. Don’t forget to take all the necessary precautions and follow all COVID-19 protocols for your own wellbeing.

Improving countryside development will allow Filipinos to grow and expand their skills, boosting productivity and economic progress throughout the country. By promoting inclusive growth in all regions of the Philippines, we can ensure that equal opportunities will be given to all Filipinos.

Contributed by: Alfonso Syquia

How Building a Credit Risk Database for Financial Institutions can Support MSMEs in the Philippines

Micro, small and medium enterprises (MSMEs) are considered the backbone of our country’s economy. They make up 99.5% of the business enterprises in the Philippines and account for 62.4% of total employment. But with the nationwide lockdowns implemented during the pandemic, they became one of the most vulnerable sectors in the country.

Unfortunately, MSMEs struggle to apply for loans. Financial institutions consider them as high risk due to their lack of credit history and accepted collateral – two major considerations for approving loans usually. The lack of access to credit makes it difficult for MSMEs to sustain their business, especially now with the pandemic.

To address this, Japan International Cooperation Agency (JICA), the world’s largest bilateral agency, and Bangko Sentral ng Pilipinas (BSP) collaborated for a financing program that will develop a statistical reference tool to promote risk-based lending. The establishment of a Credit Risk Database in our country is an important step in creating a long term support and sustainable financing ecosystem for MSMEs.

What is the Credit Risk Database (CRD) Project?

Credit Risk Database (CRD) is a financing program for MSMEs that provides them with a statistical credit scoring which can be used by lenders as a source of information to assess the borrower’s capacity to pay. It will help address the challenges of MSMEs such as their access to finance due to lack of collateral, inability to provide credit history, and banks’ lack of information in assessing credit.

What are the goals of the Credit Risk Database Project?

Launched in December 2020, 17 banks participated in the 3-year BSP program which will help create a scoring model.

Implementing CRD will enable banks to use a robust credit scoring model to validate their internal scoring models. The credit program will also help banks that lack a credit scoring model and enhance the credit risk management system in the Philippines. More institutions can extend more loans to small businesses and strengthen the efforts of the government to support MSMEs in the face of the pandemic.

Growing the MSME Sector with Easier Access to Credit

As BSP Governor Benjamin Diokno stated in his speech, the financial program will increase MSMEs’ access to credit, leading to their improved productivity to generate more jobs and source of income to more Filipinos. By building a credit risk database in the country, we can support the economic recovery of MSMEs and provide them long-term support to ensure their growth.

You can learn more about government programs that support MSMEs in the Philippines here.

Contributed by: Luisa Mae Gonzales

Digital Transformation for Financial Institutions: Unleashing Their Potential With the Right Foundation

When we think about financial inclusion, we think about the shared goal of including all members of the society to access and benefit from the same financial services accessible to more developed areas.

By supporting the digital transformation for financial institutions, we can provide accessible financial solutions to the unserved and underserved sectors in society. It can encourage better financial inclusion by giving access to basic financial services and other transactions that are more convenient.

But this transition cannot happen overnight. It takes time to provide financial access to different parts of society, especially the vulnerable and unserved populations in the country.

Despite various initiatives launched to encourage digitalization, the Philippines still finds it difficult to achieve the goal because of its weak digital infrastructure. This hinders the progress of financial institutions to shift now to the digital market.

Improving Digital Infrastructure for Better Opportunities

In order to improve the digital infrastructure in the Philippines, we should support the transformation efforts of community-based institutions properly. Rural banks, microfinancing institutions, cooperatives, and other similar financial institutions are just a few of the institutions that can serve and can reach underserved and unbanked Filipinos in need of access to basic financial services.

However, institutions need to consider several factors when it comes to digitalization.

Their goal

Before institutions can start their digitalization journey, they need to determine their goal first. What do they want to achieve? Answering this question is a crucial step for them to plan out the steps they need to take. This will ensure that they have a strong blueprint that not only addresses their pain points but also secures efficient digital transformation for financial institutions.

Proper collaboration and partnership

Once financial institutions know their transformation goal, the next step is to find the right partner that can help them in their digitalization journey.

Collaborating with the right provider can help banking and non-banking institutions establish a solid foundation. Through proper collaboration, they can optimize their processes and be equipped with digital solutions that address the digitalization challenges they experience. It will enable institutions to serve Filipinos better and bring more opportunities to their communities.

Empowering Financial Institutions with Strong Digital Foundation

Once financial institutions find the right partner with the right solutions, they can now start their digital transformation by building a digital foundation. This is a vital first step as the right foundation will ensure:

Holistic and full transformation

Digital transformation needs a strong foundation. If an institution has an improper foundation, it will take them longer and more effort to transform fully.

With a solid foundation, financial institutions can speed up their processes, optimize their workflow, and ensure better customer experience. It will also allow a smooth transition to the digital economy and provide underserved and unbanked Filipinos easier access to it.

Seamless integration and utilization of digital solutions

Based on a World Bank report, the use of various digital technologies has paved the way for citizens, businesses/companies, and the government to follow strict health protocols while still ensuring business continuity, economic activity, and being able to deliver a variety of deposit options, lending, investment services and such to the public.

When paired with the right digital foundation, it will be easier for financial institutions to integrate and use other digital solutions like agent banking and mobile banking. This would bring about greater efficiency in improving customer experience and other business processes.

Eventual expansion of rural and marginalized communities to the digital economy

With urban areas constantly booming in the digital industry, community-based financial institutions are ones that can help rural communities shift to the digital economy.

As these institutions gained the trust of their communities, they can help more people to be banked and encourage the transformation of financial services in their communities. This can improve financial inclusion as even Filipinos in poverty can have savings, apply for loans, and get financial protection.

Helping them transform would give Filipinos the chance to participate in the digital economy even if they’re in far-flung areas.

With a proper foundation, institutions can maximize their potential in serving rural and vulnerable communities in the Philippines.

Paving the Way Towards Community Transformation

Technology has proven to be a useful tool for Filipinos to access financial services safely and securely. With stores, businesses, establishments, and households heavily affected, we need to guarantee continued financial access that can help Filipinos, especially the unbanked and underserved, recover during these trying times.

As said by BSP Governor Benjamin Diokno, “The future is digital, and it is here. We need to make sure that our constituents and the public that we serve are not left behind. Let us prepare them for the new economy and equip them with access to transformative digital financial services.” By setting the right foundation for digitalization, we can find ourselves on the right path towards financial inclusion.

We have to ensure that no community-based financial institutions will be left behind. By transforming financial institutions in the Philippines, they can keep up with the latest innovations and be competitive in the digital era. Working together to build a financially inclusive system in the country can empower more Filipinos. It will help them shift to digital banking where they can access their accounts online, pay bills, transfer funds, apply for loans, and other services with ease.

The benefits of digitalization in the financial industry are never-ending. As technology continues to transform our lives for the better, we can look forward to a financially inclusive country with the right solutions to support it.

Contributed by: Pamela Belmonte